gerisima/iStock by way of Getty Photographs

Funding Thesis

Years of decrease gross sales, shrinking ROIC, and declining margins add to the numerous dangers forward for Leggett & Platt, Included (NYSE:LEG). This Dividend King might even lose its crown if their scenario does not enhance.

Bedding And Bedding Equipment

Leggett & Platt is an organization that makes varied consumer-discretionary merchandise, significantly bedding merchandise like mattress springs, adjustable beds, metal rods, and others.

Additionally they provide residence furnishings merchandise with recliner mechanisms, chair controls, and carpet cushions, amongst different issues.

They spherical out their product line with extra specialised merchandise, comparable to automotive seat help, aerospace tubing, and hydraulic cylinders for industrial and transportation use.

Leggett & Platt Firm Replace 2024

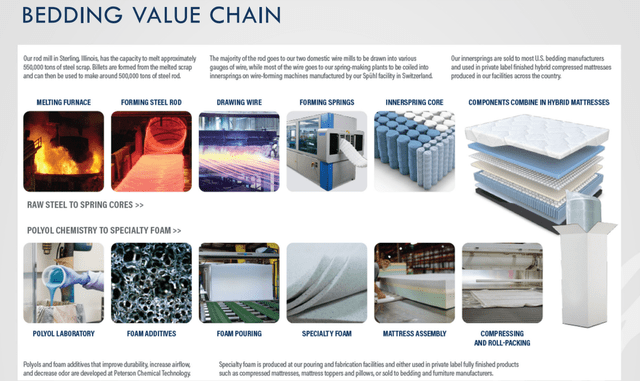

The enterprise may appear easy on the floor, but it surely truly has a comparatively lengthy worth chain that mixes many alternative supplies into bedding parts.

Lengthy worth chains are extra complicated to copy by newer opponents and thus can additional widen an organization’s moat, particularly with specialised know-how and extra commerce secrets and techniques.

Leggett & Platt Firm Replace 2024

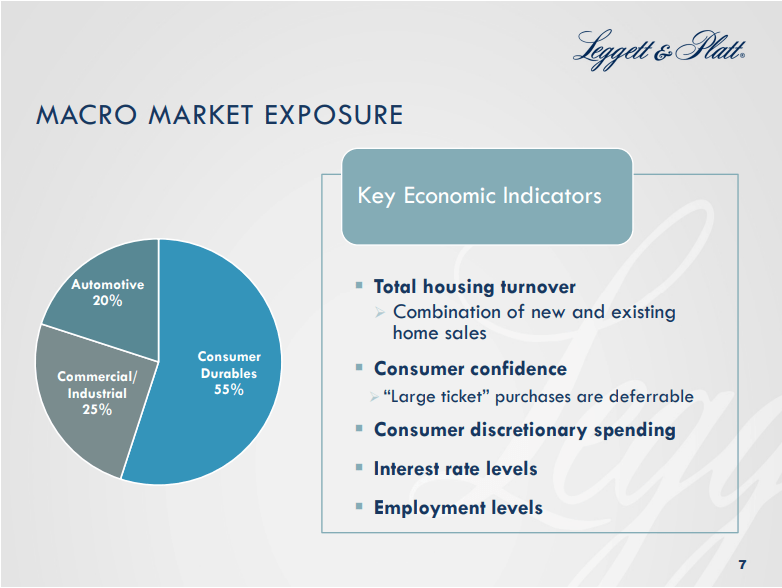

LEG is definitely a slightly diversified firm, as they’ve services that produce bedding parts for family use, automotive seat help, and even tube assemblies for the aerospace trade.

This diversification is constructive, as the corporate can pivot into different areas extra rapidly than extra specialised firms; it additionally opens up new alternatives for exploitation.

I consider it may well profit an organization with broader experience and will ultimately result in cross-innovations among the many totally different product strains. For instance, if the automotive division develops a extra comfy sort of lumbar help, LEG might extra simply translate this right into a furnishings or bedding product.

Having totally different sectors with totally different wants, comparable to business/industrial, client, and automotive, may also help an organization be extra strong when a specific sector is going through issues.

I price this as a web constructive for the corporate.

Cash By no means Sleeps

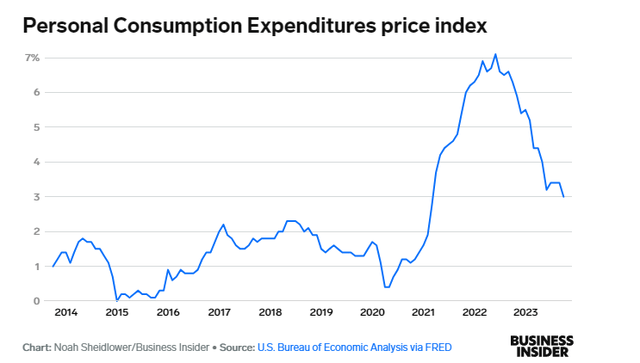

LEG is going through a tough patch in its gross sales. The patron sector of family durables is extra susceptible to inflation and decrease client expenditure than different client sectors. With lower demand for goods, furnishings, and family durables, tendencies depend upon a extra constructive financial surroundings.

Enterprise Insider: Chart: Noah Sheidlower/Enterprise Insider Supply: U.S. Bureau of Financial Evaluation by way of FRED

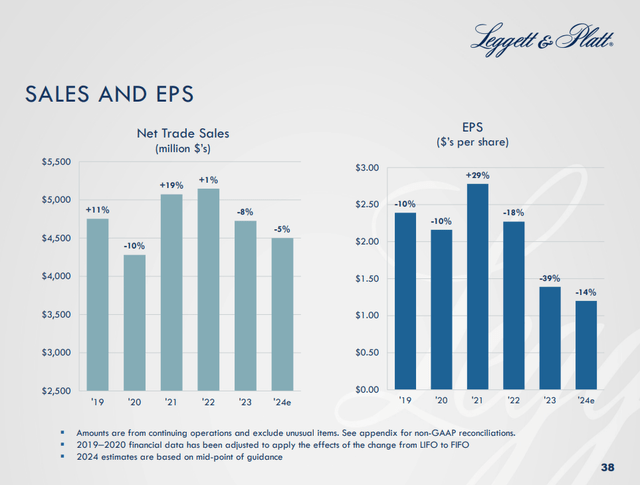

LEG has been a sufferer of this, having 2023 with a 7% lower in gross sales and a 3% decrease quantity. The yr 2022 wasn’t that sizzling both, with a 1% improve in gross sales vs. 2021 and seven% decrease quantity. Development is sorely missing for LEG. The corporate expects 2024 to be one other yr with decrease gross sales and quantity, starting from 2% to eight% decrease gross sales and a quantity drop within the single digits.

Leggett & Platt Firm Replace 2024

We are able to see the correlation between client expenditures and LEG’s gross sales and EPS. The corporate wants a positive development.

That is most likely the one fundamental issue that influences the remaining. LEG shouldn’t be in a constructive secular development; the falling gross sales want a turnaround earlier than it is too late.

Metal, Wool, And Wooden, The Fundamentals Of Sturdy Beds

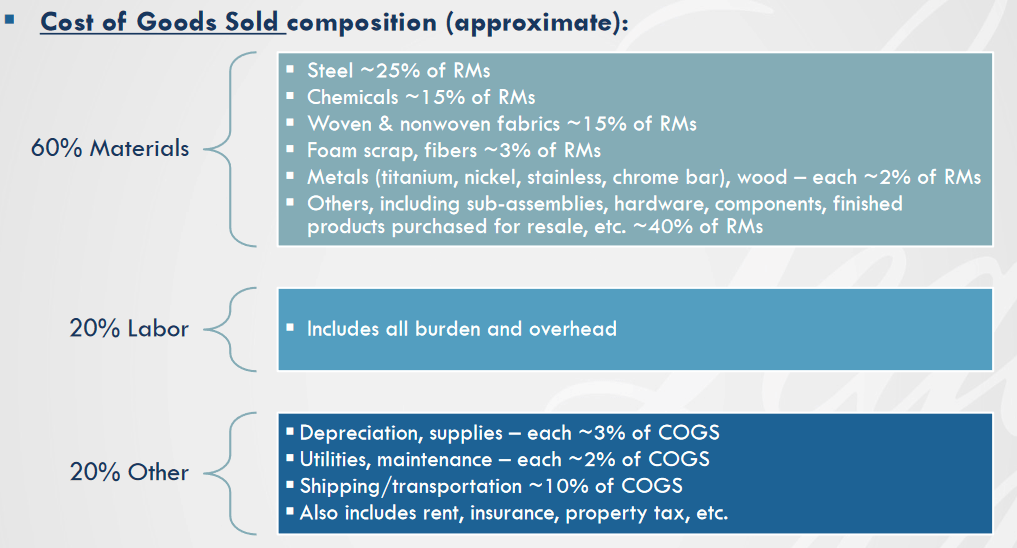

As beforehand acknowledged, LEG has a slightly lengthy worth chain that takes metals, fiber, plastics, chemical substances, textiles, and foam scrap and turns them into both comfy residence and work furnishings or helpful automotive, industrial, or aerospace parts.

The lion’s share of the prices of products, after all, comes from supplies, with 60% of the prices, in reality, with 15% of the general prices of products coming from metal.

The corporate’s publicity to danger comes within the type of market fluctuations that might push the value of the required supplies into an unsustainable vary. Steel, in particular, appears to be a chief goal for tariffs and business conflicts between its main producers.

Leggett & Platt Firm Replace 2024

I price this as a doable danger that might compound the opposite issues and preserve pushing the profitability targets additional away.

The Comforts Of Effectivity

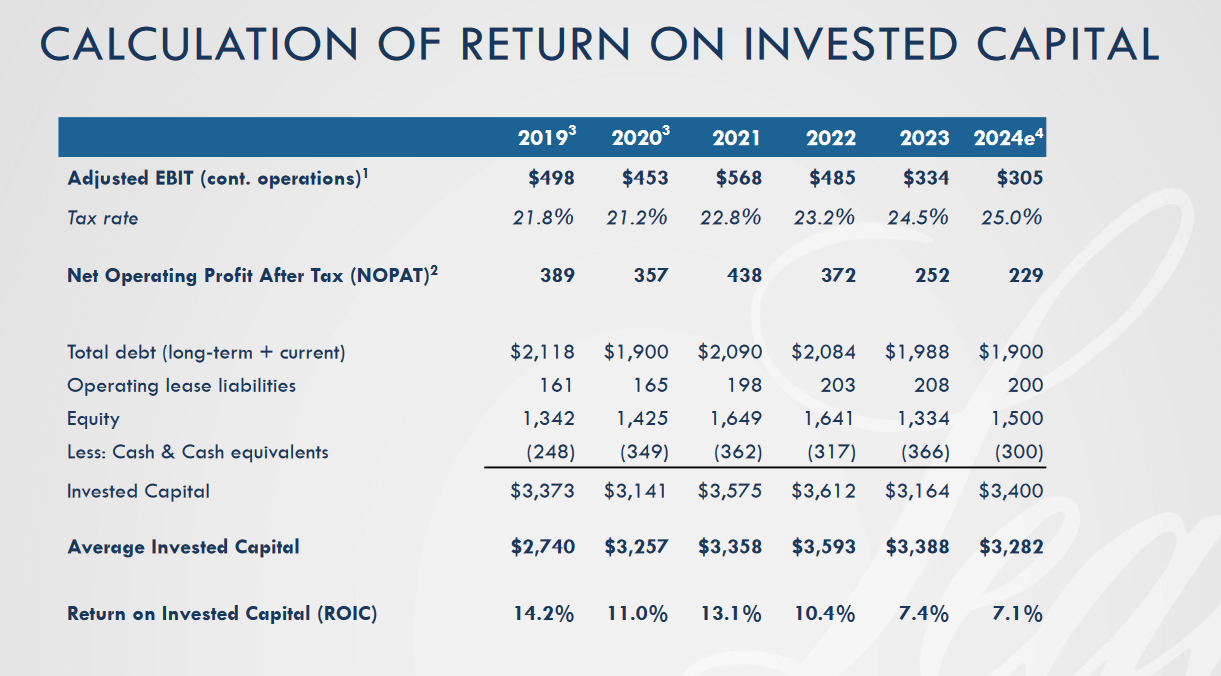

LEG shouldn’t be in a snug place proper now, with issues in its capability to show gross revenue into web earnings.

Leggett & Platt Firm Replace 2024

The ROIC, an important metric for understanding how effectively an organization is utilizing its capital, has been on a gradual downtrend since 2019. This isn’t one thing buyers wish to see. Ideally, an organization would improve its ROIC with time because it streamlines its operation and negotiates higher offers with suppliers and patrons, amongst different issues that enhance the margins.

Evaluating the ROIC with the WACC, we are able to perceive whether or not or not the corporate is creating worth. With a WACC of 7.51%, LEG shouldn’t be creating worth in the mean time.

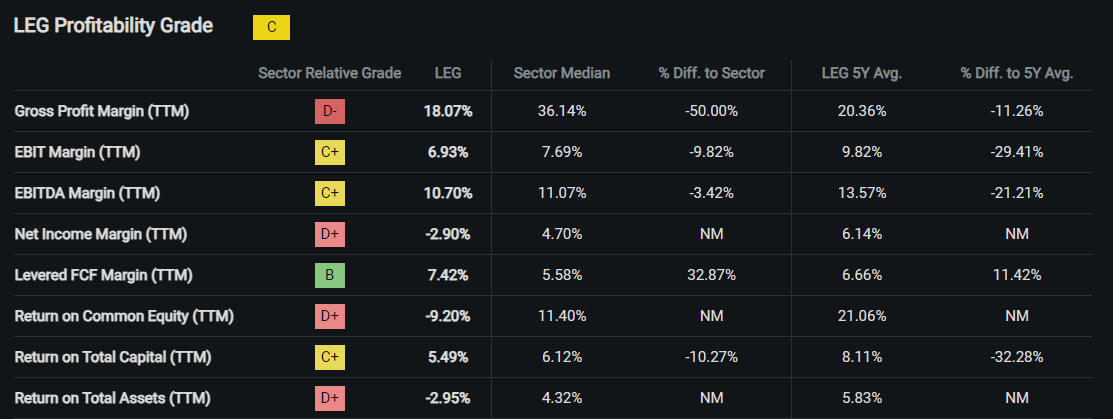

Looking for Alpha Quant

Their gross revenue margin is 50% decrease than their friends, and the ROTA (return on whole property) is -2.95%. Nevertheless, the levered FCF margin is 32.87%, superior to the sector’s.

Whereas the corporate has points with a low gross revenue margin and a destructive ROTA, at the very least it retains money after paying all money owed at a better stage than different firms in its sectors. General, the image shouldn’t be very constructive, and LEG at present depends upon the success of the restructuring plan to turn out to be worthwhile once more.

The Restructuring Plan

LEG’s administration has acknowledged the corporate’s scenario and has taken steps toward a bold restructuring plan. The plan focuses on innovation and better worth, particularly within the bedding merchandise space. Whereas chopping down on much less worthwhile places, this leaning down will convey LEG from 50 manufacturing and distribution places to round 30 to 35.

I consider this can be a step in the fitting course for any firm going through unfavorable headwinds and decrease margins. It ought to take steps to cut back prices and concentrate on creating extra worth.

This plan could take till 2025 to finalize, though there’s at all times the danger of delays when attempting to chop down.

This is among the greatest gross sales factors for any bullish thesis on LEG, but it hinges on the corporate finishing this course of and ending up with a extra environment friendly, extra streamlined enterprise.

The need of this plan is obvious from the earlier factors. Nonetheless, I do consider this will doubtlessly compound the dangers forward for LEG, as any vital delays might delay the date of lastly having a worthwhile enterprise.

2024 will most likely be one other yr with destructive progress, so LEG should actually make the restructuring plan go proper in the event that they purpose for constructive progress in 2025.

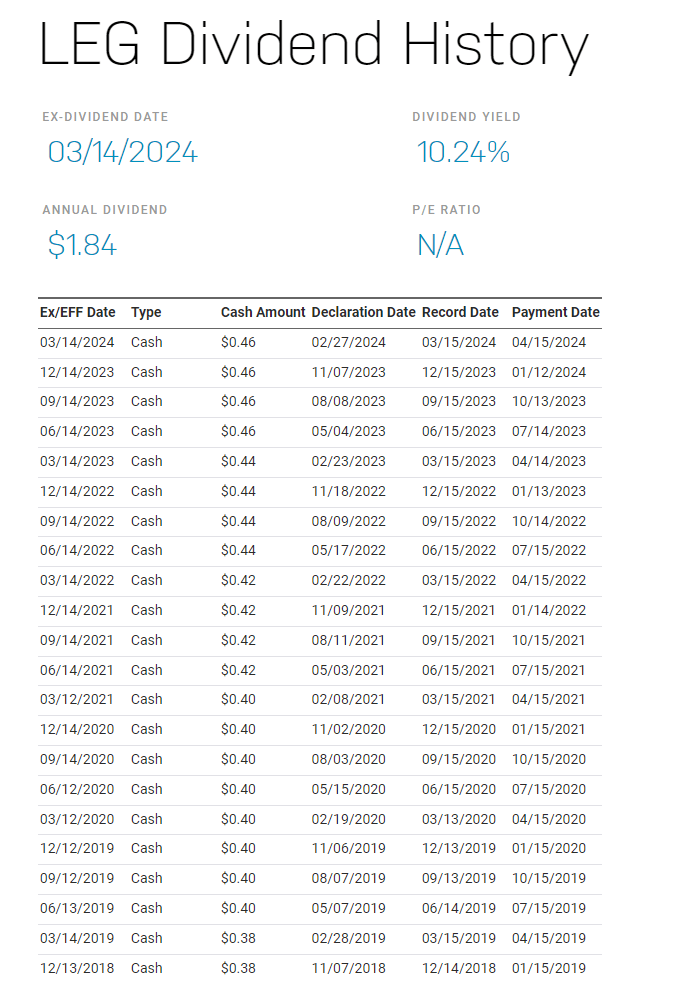

A Dividend Worthy Of A King

Uneasy lies the top that wears a crown.

-William Shakespeare

LEG is a dividend King, which implies that as a substitute of “simply” 25 years of rising dividends, it has been rising their yearly dividend for 50 years straight.

In regard to the dividend elite, most dividend aristocrats and kings would not have exceptionally excessive dividends. As an alternative of upper yields, buyers can discover the security of a protracted monitor file in a mature firm.

Right here, LEG stands out, because it at present has the best dividend yield of the dividend kings, 9.69%, which is 3.4X occasions above the Kings’ common yield of two.85%.

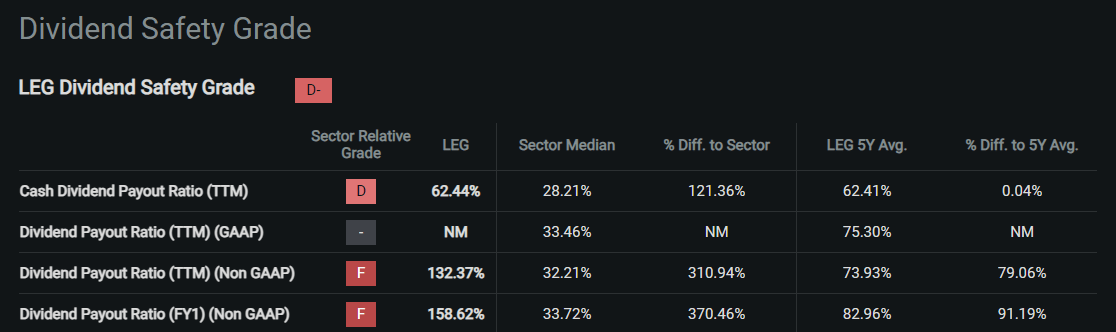

The corporate has a Dividend Per Share of $1.82 and Earnings Per Share of $-1; clearly, the dividend shouldn’t be lined. Furthermore, the standing of LEG as a part of the dividend elite is threatened. The corporate has low and even destructive prospects for earnings progress and a payout ratio of -182% if we use Earnings.

Earnings are a tough measure of what the corporate makes in a yr, they usually embrace many gadgets that aren’t essentially a very good measure of the corporate’s efficiency.

Looking for Alpha Quant

Utilizing the Money Dividend Payout Ratio or the Dividend Payout Ratio (Non-GAAP), LEG remains to be means worse than its friends. The decrease finish of the size locations LEG at 370.46% worse than its opponents when it comes to its capability to proceed funding the dividend.

I consider Looking for Alpha Quant’s Security Grade of D- is an apparent signal that the dividend is likely to be enticing for its yield however needs to be intently monitored for its security, lest it turn out to be a dividend lure.

It’s a huge risk that the inventory would plunge if the dividend king class have been misplaced, which is a real risk, contemplating the earlier lack of gross sales progress and shrinking margins.

NASDAQ Web site LEG Dividend Historical past

Primarily based on its historical past of dividend raises, I consider LEG will proceed in 2024 with a dividend elevate of 0.02 and in 2025 with the same 0.02 elevate, thus sustaining its dividend king standing however worsening the corporate’s total monetary scenario.

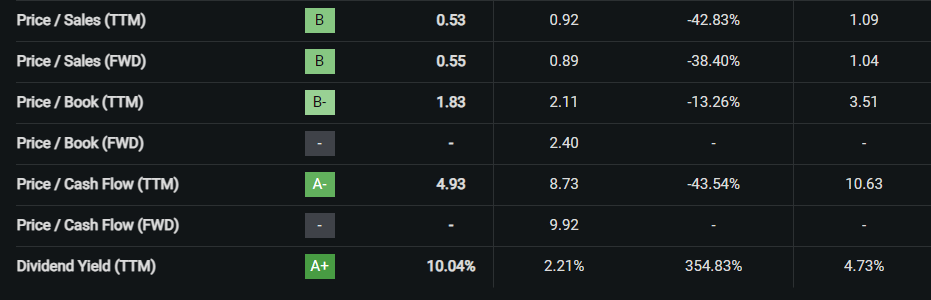

The Most cost-effective Dividend Yield Amongst The Dividend The Aristocracy

Valuation is the place any funding thesis in favor of LEG shines. The corporate has the most cost effective dividend yield pound-for-pound of any Dividend King.

Looking for Alpha Quant

The corporate gives a gorgeous valuation in comparison with its peer in 4 key areas:

- Value To Gross sales

- Value To Money Circulate

- Value To E-book

- Dividend Yield

The Value To Gross sales may be very enticing at 0.55, 38.40% beneath the remainder of the sector; the Value To E-book stands at 1.83, and the value to money movement can be low at 4.93, making it 43.54% cheaper than its friends.

From this, we are able to say that the LEG inventory gives an fascinating valuation in a few of a enterprise’s most vital areas. I feel the 2 greatest issues to contemplate are the low value to gross sales and low value to money movement, as each are two of a very powerful issues that needs to be thought of when shopping for a inventory.

Up to now, comparable to within the dot-com bubble, when sky-high costs of shares have been the norm, glancing at how a lot a doable purchaser would pay for every greenback, the corporate made in gross sales might have helped keep away from a number of the worst examples of overvaluation.

The identical factor applies to Money Circulate. As Warren Buffett says, “Money is King.” Paying much less for more money movement is at all times higher, and once more, in bubbles, firms could have insane valuations, with patrons paying for every money movement greenback within the dozens and even lots of.

The Value To E-book can be a web constructive for LEG; as an organization that produces items, a low P/B proves that we aren’t in entrance of a string of pricey (to buyers) buildings and machines.

Many buyers may very well be considering now: “However is not worth investing about discovering low cost shares?”

To cite Warren Buffett: “It’s miles higher to purchase a beautiful firm at a good value than a good firm at a beautiful value.”

LEG’s enticing ratios are based mostly on comparisons with the remainder of the market, comparable to a Value to Gross sales of 0.52 and a ahead P/E of 13.91, however in gentle of the corporate’s total efficiency, it’s clear that we’re, in reality, in entrance of a dropping firm with a comparatively low value and never an excellent enterprise at a good value.

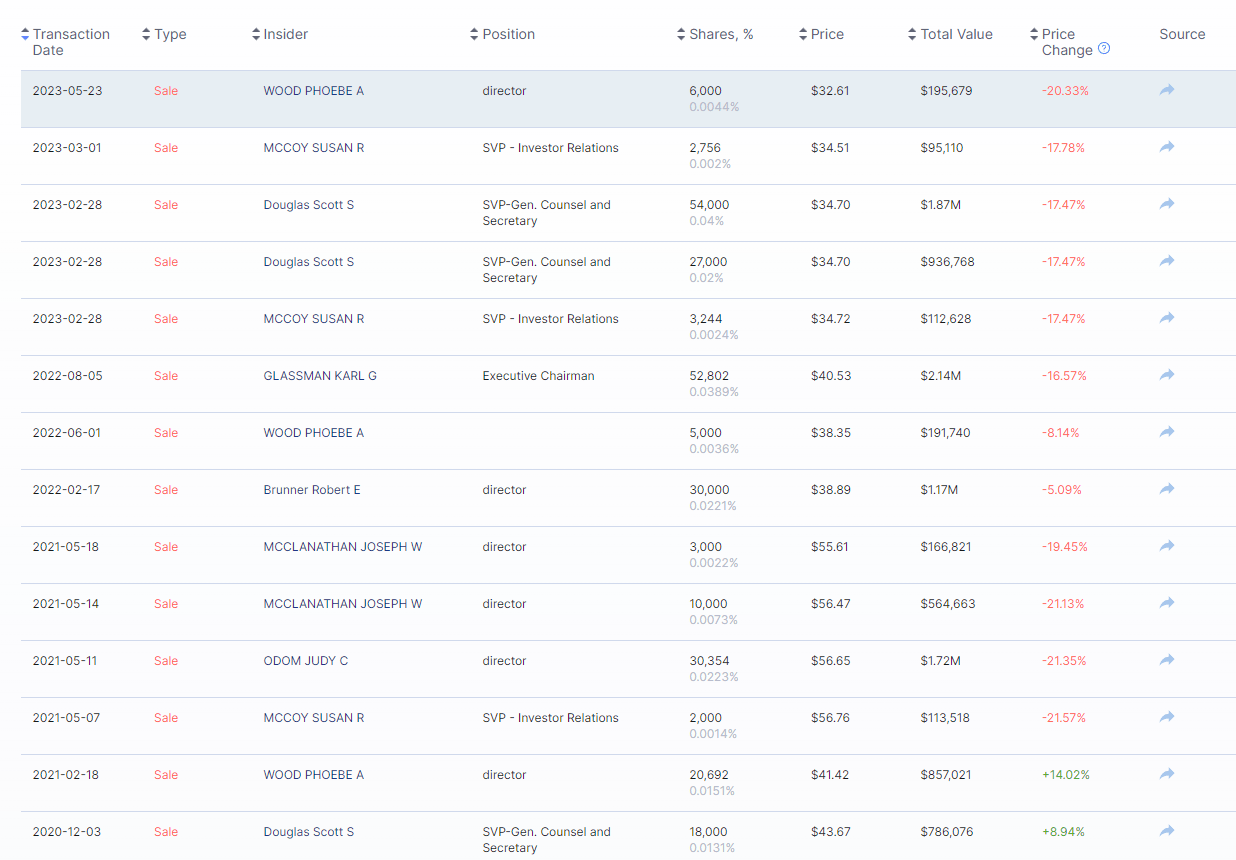

Insider Buying and selling

My curiosity peaked once I noticed the time period “Pores and skin within the sport,” which Warren Buffett popularized. It refers back to the significance of aligning the corporate’s higher-ups’ incentives with the enterprise. I made a decision to do a fast search of inventory buying and selling by administration. After all, this data is public and must be registered with the SEC.

Leggett & Platt COMPANY UPDATE November 2023

I made a decision to look and see how many individuals on this firm have been buying and selling the inventory. In reality, I had to return to 2015 earlier than I might discover a purchase. Now, promoting inventory by administration is a pure and regular a part of enterprise. Many complement their wage with the gross sales of their inventory compensations, however it may well convey into query how a lot pores and skin within the sport administration actually has.

Prismo.professional

Rivals

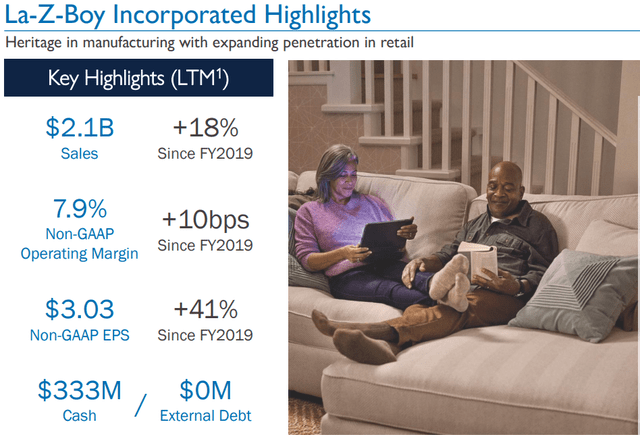

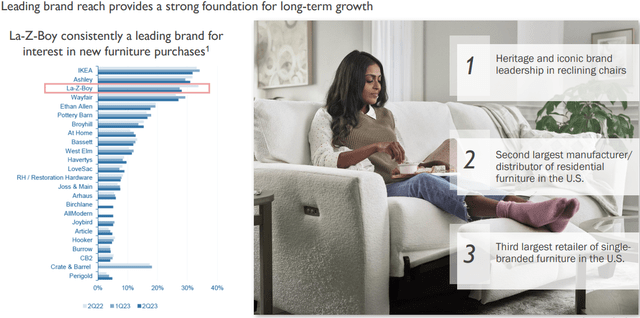

Their greatest rival might be La-Z-Boy (LZB), an organization with fairly sturdy branding and rising gross sales since 2019.

LA-Z-BOY Investor Presentation

In reality, the biggest energy of LAZB is its highly effective model, which it might proceed to leverage with the aim of frequently rising its market share.

LA-Z-BOY Investor Presentation

One benefit LEG has over LAZB is its broader diversification, which might permit pivoting for LEG if the competitors begins consuming into its market share.

But, the case stands that LEG has a reasonably sturdy rival, with superior branding and rising gross sales.

Capital For Innovation, Capital For Rising

Because of the lack of gross sales progress, decrease ROIC, and the excessive dividend that should be paid, there’s a actual likelihood that money will movement in an ever-greater proportion in the direction of dividends and away from the required CAPEX and high-quality acquisitions that might assist the corporate innovate and develop.

Leggett & Platt COMPANY UPDATE November 2023

If the restructuring plan doesn’t come to fruition within the scheduled time and throughout the limits of the funds, this might as soon as once more compound all of the earlier issues and would possibly begin a spiral that might require extra drastic measures.

I price this as probably the most vital danger for the corporate.

Conclusion

I price LEG as a SELL. The valuation is likely to be low cost, however the prospect of years forward of destructive progress, years of returns and margins on a downtrend, and a combination of danger actually make this inventory a SELL for me. I feel all of the earlier issues can doubtlessly pile up on one another and preserve dragging this firm down.

The margin of security might turn out to be extra enticing in time, and if the situations enhance and progress materializes, a revision may very well be so as.